Real Assets

We build future energy systems and resilient infrastructure, backing emerging opportunities in technology, land and water.

The energy shocks of the 1970s came in two waves. The 1973 Oil Embargo exposed how vulnerable oil importing economies were to external geopolitical forces. The 1979 Iranian Revolution then removed any illusion that this vulnerability could be managed without far-reaching adjustments.

For Western economies, the 1970s revealed energy security to be a foundational input to economic stability and social cohesion. In the UK, for example, the decade was marked by industrial unrest and economic instability, culminating in its Winter of Discontent. More broadly, what followed from these shocks was a fundamental shift in how Western economies approached energy. Energy security moved to the centre of economic policy. Governments prioritised diversification, accelerating the development of domestic resources such as the North Sea and supporting alternatives including nuclear and coal. At the same time, managing demand became as important as securing supply. Improvements in energy efficiency, changes in industrial structure and a move away from oil in power generation led to a sustained decline in oil intensity across OECD economies.

The geopolitical upheavals of the past few years bear a striking similarity to the two shocks of 1970s. In 2022, Russia’s invasion of Ukraine exposed the extent of Europe’s dependence on imported energy. This triggered a sharp rise in energy prices and prompted a rapid policy response focused on diversifying supply, reducing demand, and accelerating domestic clean energy investment. The current war in the Middle East, the second energy shock of the 2020s, has yet again exposed the same underlying vulnerability, only this time with broader implications for global oil and gas flows. For many Asian economies – the main customer for Middle Eastern energy – the impact is likely to be more immediate and acute, with higher oil and LNG prices feeding directly into transport and industry and reinforcing the case for electrification and greater investment in domestic energy capacity.

Where the first shock of the 2020s was largely European, the current disruption is global and likely to drive lasting change.

Having been established in the aftermath of the 2022 Russian invasion of Ukraine, Europe’s plan to counter this latest energy shock is well-established. The ultimate endgame is a fundamentally European one: reduce dependence on imported energy and build an energy system that can be supported and supplied domestically.

In the near term however, countering energy shocks has meant diversifying energy supply. Having weaned itself from Russian pipeline gas, Europe now relies heavily on Norway and the US for energy. The continent is now the world's largest importer of LNG with its single biggest supplier being an increasingly antagonistic US. With countries such as Germany currently sourcing as much as 96% of its LNG from the US[1], a reliance on outside actors for energy supplies exposes Europe to yet new wildcards. Simply removing Russia from its list of suppliers therefore has not solved Europe’s energy security concerns. Moreover, this new European reliance on LNG has made it similarly vulnerable to global price volatility in times of geopolitical crisis. Diversifying energy supply remains only a partial solution therefore as while the continent has successfully reduced reliance on one supplier, it has maintained an exposure to global fuel markets.

The more durable response to this latest energy crisis is the continued structural change to deploy clean energy and reshape energy demand. Since 2022, policy and capital have been mobilised at scale. REPowerEU alone committed around €300bn to support the green transition[1]. The impact of these policies is beginning to become visible. Renewable generation has increased materially, rising from around 30% of EU power supply to close to 50% today[2].

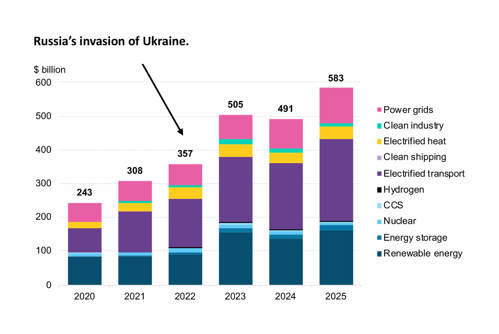

Figure 1: Energy transition investments in Europe by sector, 2020 to 2025[1]

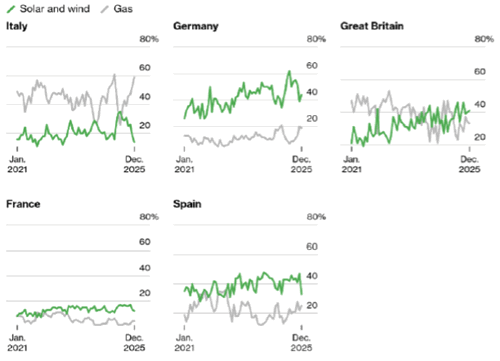

At the same time, the structure of the power system is beginning to change. Greater renewable penetration and structurally lower demand have weakened the link between gas prices and electricity prices. Gas remains a key risk factor, but its influence now varies significantly between markets. For example, supported by rapid renewables development, gas has influenced Spanish power prices in only around 15% of hours so far in 2026, compared to 89% in Italy[1].

Figure 2: Share of renewables and gas in power generation, 2021-2025[1]

Europe understands that it cannot subsidise its way through repeated energy crises indefinitely, particularly given the fiscal pressures created by the COVID-19 pandemic, the 2022 energy crisis and rising defense spending. The adjustment therefore must come from reducing demand for fossil fuels rather than offsetting their cost. Technologies that can be deployed quickly and at scale to achieve this, particularly co-located solar, storage and offshore wind, are likely to benefit. The plan and direction have been clear since 2022 and the current shock will simply force Europe to move further and faster.

For many Asian economies, this energy shock will be more acute than Europe’s experience in 2022. Around 80% of the oil and 90% of the LNG that passes through the Strait of Hormuz is destined for Asian markets[1]. Asian economies remain heavily dependent on imported fossil fuels, often with limited domestic production and relatively low strategic buffers. This leaves them highly sensitive to disruption and price volatility.

The early Asian response reflects this vulnerability. Governments across Southeast Asia have already begun implementing demand-side measures like those seen in Europe in 2022 and, further back, in the 1970s. Four-day working weeks, remote working mandates and fuel conservation policies are being introduced to reduce consumption, while subsidies are being expanded to cushion the impact on households and industry. Vietnam and the Philippines, for example, who import 95% and 88% respectively of their crude oil from the Persian Gulf have already disbursed over $560m to subsidise fuel costs[2]. Moreover, Vietnam has exempted nearly all fuel taxes during this period, reducing its state budget by an estimated $277m per month[3]. The scale of these unsustainable interventions underscores the growing fiscal burden of shielding consumers from volatile fuel costs and the risks of reliance on imported fuels. More structurally, the region is exposed to the mechanics of the global energy markets in a way that is difficult to hedge against. With oil priced globally, in period of tight supply, wealthier economies such as those in the West will be able to secure cargoes at higher prices. This will force price-sensitive importers to reduce demand, whether it is painful or not.

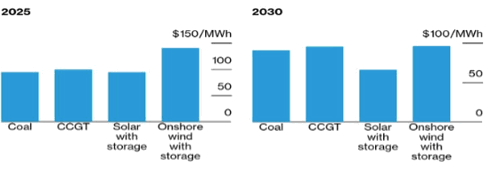

However, this crisis arrives for Asia at a different moment in the energy transition. Unlike the 1970s, and even compared to Europe in 2022, viable alternatives to imported fossil fuels are available at scale. Solar plus storage now costs $60/MWh at a global level, while the variable cost of LNG exceeds $160/MWh[4]. Technologies including solar, wind, batteries and EVs are now cost-competitive and deployable at scale, offering a clear pathway for Asian countries to reduce export dependence structurally rather than temporarily.

Figure 3: Levelised cost of electricity of new power plants in the Philippines, in 2025 and 2030

Asia’s current position is complex. The short-term adjustments forced by the closure of the Strait of Hormuz are likely to be disruptive and psychologically scarring. However, the long-term opportunity through structural changes is clear. Electrification and domestic renewable development will offer a route not only to improved energy security but also retaining more value within their economies. This creates a dynamic like that seen in Europe, but with a different starting point and trajectory.

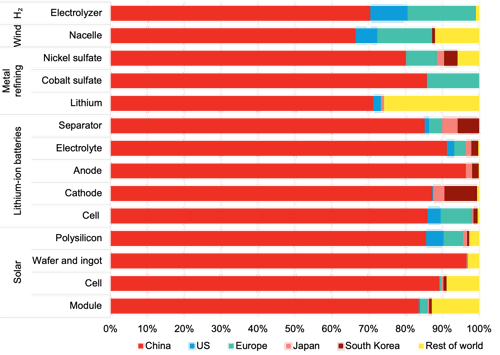

A decade of renewable build-out and electrification has materially reduced China’s exposure to energy shocks. Moreover, the country’s long-term focus on electrification has positioned it as the world’s largest producer of clean tech. The ability to sell nations the equipment required to diversify their energy mix gives China a unique leverage on governments intent on weaning themselves off Middle Eastern imports. However, this shift risks introducing a new form of dependency where reliance on Middle Eastern fuels is exchanged for a reliance on Chinese clean technology components. How should nations respond if access to critical clean technologies becomes contingent on alignment with the policy priorities of supplier countries?

Figure 4: Clean-energy production capacity, 2023[1]

For a genuine structural change, this dynamic must be approached globally through policy response. The US had begun to address it through the Inflation Reduction Act, but that momentum has become less certain. In Europe, concerns over strategic dependence are already translating into more protectionist measures, including local content requirements and support for domestic manufacturing. Across Asia, there must be a push to build out local clean energy industries, both to capture economic value and to reduce exposure to external suppliers.

Even so, the nature of this new dependency is fundamentally different. Fossil fuel systems require continuous imports, with supply disruptions feeding through into the economy within weeks. Clean technologies, once deployed, provide energy for decades with no ongoing fuel requirement. A country may face constraints in maintaining or expanding its system if supply chains are disrupted, but it is far less exposed to sudden, system-wide shocks.

The oil shocks of the 1970s are now understood as a defining pivot in the creation of the modern energy system. They forced economies to confront the limits of cheap, imported energy and to redesign their energy systems around security, diversification and efficiency. The effects were not immediate but viewed across the decades they were lasting and clear.

With the first energy shock of the 2020s exposing a vulnerability, and the second making it clear that the vulnerability was structural, a similar dynamic to the 1970s has emerged. What is different this time is that the structural adjustment emerging is truly global. Europe has been on a clear path since 2022, while Asia is now being forced to confront its acute vulnerabilities as an importer of fossil fuels. Moreover, China offers a glimpse to where this process may lead but also highlights the new opportunities and risks that come with it.

What is clear is that repeated energy shocks reshape economies. The changes triggered by the shocks of the 2020s will not be fully understood for years, but, as in the 1970s, they are likely to define the trajectory and structure of the global economy for decades to come.