Real Assets

We build future energy systems and resilient infrastructure, backing emerging opportunities in technology, land and water.

The EEG drove massive solar installation growth but the mechanism simply folded the subsidy into the consumer retail price and soon this became a noticeable inflationary cost factor to the dismay of the German retail electricity customers. Solar PV had become an unsustainable money-sapping villain.

Fast-forward to 2026 and Chinese solar panels prices retail in the $0.1-$0.2/Wp range and unsubsidised solar power has become one of the cheapest electricity sources on the planet together with onshore wind. And as we will see, this is just in time since the “electrification of everything” megatrend is creating huge demand pressure on the electricity grid, especially in the US.

The world is warming and a powerful solution lies in parallel actions to “electrify everything” while decarbonising electricity generation. The first part of this journey actually started centuries ago (thanks to clever physicists like Michael Faraday, Alessandro Volta, Nikola Tesla, and James Clerk Maxwell) while decarbonisation began in earnest in the 2010s and was given extra impetus by the Paris Agreement in 2015.

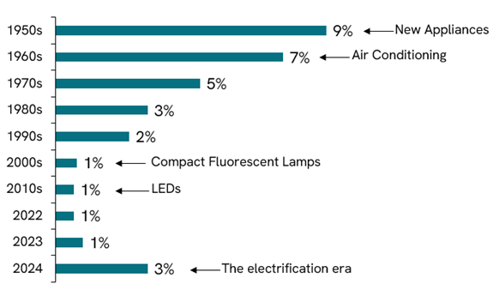

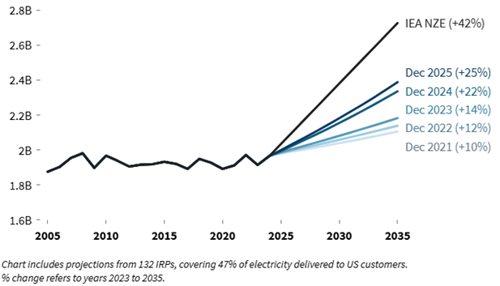

For the past few decades, continuous improvements in the energy efficiency of products resulted in an only very gentle rise in US grid load demand of around ~1% annually which was relatively easily covered. However, grid load growth has been accelerating in recent years and in 2024 we saw growth well above 1% (see figure 1).

Figure 1: Accelerated electrification generates increased electricity needs

Average annual grid load growth (US)1

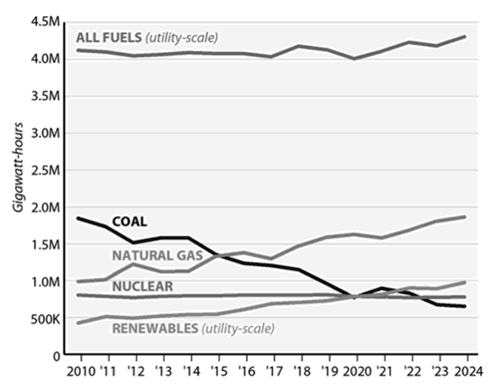

US electricity generation, GWh2

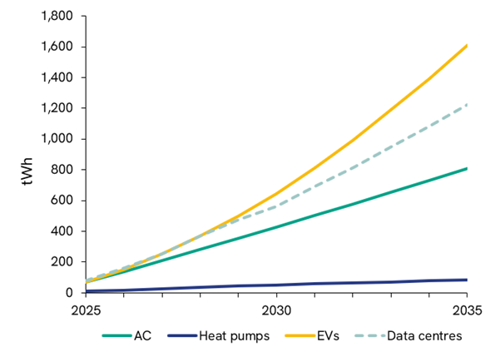

This increase is not an outlier but just the first step to an acceleration in grid load demand growth that is expected to persist for years or even decades. The reason? Shorter term, we have the rapid expansion of AI and associated need of more data centres and processing power. But as the figure 2 shows, other megatrends are also expected to play an increasingly important role, such as:

Integrated resource plans (IRPs) - essentially long term plans - from US electric utilities are also predicting progressively higher demand each year (see figure 2).

Figure 2: Electricity demand drivers and anticipated load growth upwards revisions

Global power demand growth by source3

Electricity demand in IRPs (MWh)4

And we are only at an early innings on the electrification journey. According to the IEA World Energy Outlook 2025, electricity amounted to just ~21% of the world’s final energy consumption.5 Some segments are well advanced such as the electrification of lighting (95% complete) while global transport is still at only a single digit level of electrification .

As the above charts show, the electricity demand ‘crunch time’ has started and is expected to only get more intense in coming years. Electricity prices across the US have already been rising above historic inflation level6 which adds to the pressure.

Experts are very clear on the long-term solutions needed to move towards a carbon emission-free world. This is a system-level solution comprising a large amount of wind and solar combined with various short- and long-duration storage options (battery, green hydrogen, pumped hydro) as well as potentially (small scale) nuclear (SMR), bio-energy and CCS (Carbon Capture and Storage) to complement.7

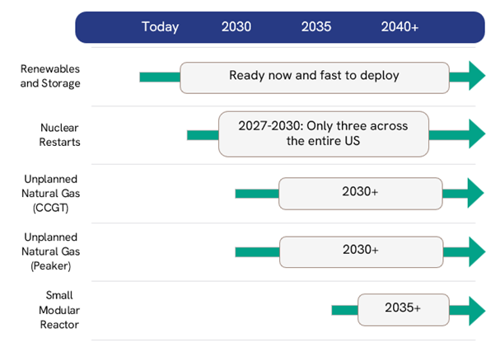

But US peak power demand is forecast to rise by ~120GW over the coming five years8 and there are currently only single digit GW of non-renewable energy generation additions under constructions or in active planning.9 This means that by far the largest share of net additions has to come from renewable energy (wind/solar) – it is the only technology that can be rapidly deployed at scale as the figure below shows . Energy efficiency is also continuing to play a role here - both in reducing demand increase but also in providing ‘new’ sources of electricity from existing inefficient processes.

Figure 3: Expected deployment timelines by generation type10

This is in fact a continuation of an already existing trend: in 2024, 92.5% of global total power capacity expansion came from renewable power sources!11

In addition to speed of deployment, onshore wind and utility-scale solar are also the cheapest sources of new electricity generation on their own and will soon be the cheapest even when accounting for storage (see figure 4 below) shows. This bodes very well for future growth of renewable energy deployment and makes us optimistic on the growth trajectory of utility-scale projects.

Figure 4: Levelised cost ranges for various energy sources (in US$ / MWh)12

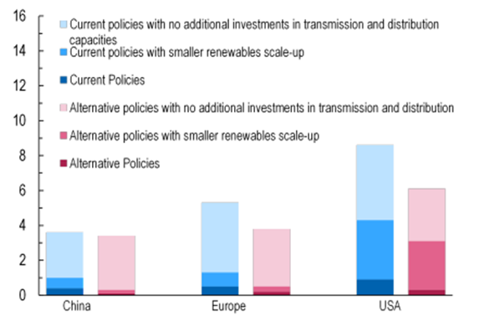

The positive impact of renewable energy on electricity prices has also been emphasised by recent analysis by the International Monetary Fund. In this analysis, the impact of rising electricity demand from data centres creates upwards price pressure but an accelerated deployment of renewable energy (red bars) abates this trend regardless of region.

Figure 5: Forecast change in electricity prices, 2030 (%)13

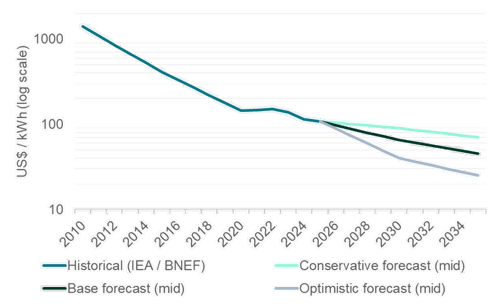

Not everything is plain sailing though. Solar/wind are intermittent energy sources and as their deployment rises, it creates risks to grid reliability. The solution is pairing intermittent renewables with battery storage. While this increases the cost, battery prices have been in rapid decline for more than a decade which means that a solar/battery system is already competitive with gas peaker power plants needed to cover spikes in electricity demand.14 As battery prices continue to fall, this technology is expected to replace new natural gas combined-cycle plants (see figure 6 below) since in many scenarios, a battery pack price in the $60-80/kWh would the cheaper option.15

Figure 6: Battery pack prices (2010-2025) and forecast scenarios to 203516

What once was a tree-hugger’s idealistic dream has become a concrete reality. Today renewable energy is fully competitive with fossil fuel technologies and indeed is the only viable solution to the imminent load grid pressures from rapidly rising electricity demand. The WHEB strategy is well positioned to continue benefitting from this development with our holdings in First Solar, Nextpower, and Vestas.

When I initiated on the solar energy sector back in 2005, I chose the title “Rise of a new power generation”. The little toddler has grown into a fine adult.

Ben Kluftinger

Senior Manager, Investments

Foresight Capital Management

Foresight Group LLP does not offer legal, tax, financial or investment advice and the information on this website should not be construed as such. We recommend investors seek advice from a regulated financial adviser. The opportunity described in this document may not be suitable for all investors. Any such investment decision should be made only on the basis of the Fund scheme documents and appropriate professional advice.

Foresight Group LLP acts as investment manager and is authorised and regulated by the Financial Conduct Authority with Firm Reference Number 198020 and has its registered office at The Shard, 32 London Bridge Street, London SE1 9SG.

OEICs

An investment in FP Sustainable Future Themes Fund, FP Foresight Global Real Infrastructure Fund, FP Sustainable Real Estate Securities Fund, FP UK Infrastructure Income Fund or FP WHEB Sustainability Impact Fund and FP Foresight Diversified Real Assets Fund (together the “Funds”) should be considered a long-term investment that may be higher risk. Portfolio holdings are subject to change without notice.

The Authorised Corporate Directors FundRock Partners Limited (registered office at Hamilton Centre, Rodney Way, Chelmsford, England, CM1 3BY) are authorised and regulated by the Financial Conduct Authority with Firm Reference Numbers 469278 and 518552 respectively. The Funds are incorporated in England and Wales.

ICAVs

An investment in the WHEB Sustainable Impact Fund and the WHEB Environmental Impact Fund (together the “Funds”) should be considered a longer-term investment that may be higher risk. Portfolio holdings are subject to change without notice.

The Manager of the Funds is FundRock Management Company S.A., authorised and regulated by the Luxembourg regulator to act as UCITS management company and has its registered office at Airport Center Building, 5, Heienhaff, L-1736 Senningerberg, Luxembourg.

We respect your privacy and are committed to protecting your personal data. If you would like to find out more about the measures, we take in processing your personal information, please refer to our privacy policy, which can be found at http://www.foresight.group/privacy-policy.