Real Assets

We build future energy systems and resilient infrastructure, backing emerging opportunities in technology, land and water.

Inheritance Tax (“IHT”) planning has always been a complex and sensitive area of financial advice. For years, advisers have wrestled with client inertia, regulatory uncertainty and the challenge of balancing tax efficiency with flexibility. Our latest research confirms that these issues persist, but the stakes have arguably never been higher.

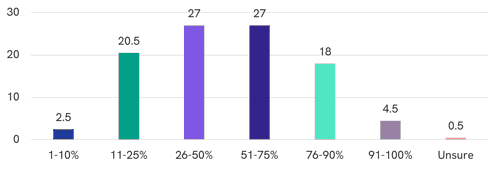

Recent pension rule changes have amplified the urgency. Half of advisers now say that at least 50% of their client bank is impacted by recent changes to IHT and nearly a quarter report that three out of every four clients are affected. Yet despite this widespread exposure and the imminent demolition of UK intergenerational wealth, only 30% of adviser clients have taken action on IHT planning, even though 68% have discussed it. That’s a huge gap and a significant challenge that needs to be addressed to help clients and beneficiaries avoid the destruction of their family's wealth.

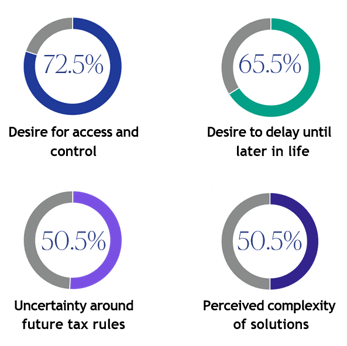

The numbers tell a clear story. Advisers are talking about IHT, but many clients aren’t moving forward. Why? Our research highlights four major blockers:

These barriers aren’t new, but they are becoming more entrenched as clients face competing priorities and a volatile policy environment. For advisers, this creates a dual challenge: how to simplify the conversation and how to offer solutions that meet clients’ need for flexibility.

The intergenerational transfer of assets will be one of the defining financial trends of the next decade. Ultimately, clients want to preserve wealth for their beneficiaries without losing control during their lifetime. Advisers who can position estate planning as a way to retain family assets and futureproof financial security will strengthen relationships across generations and build and retain assets.

Yet inertia remains a risk. If clients delay planning, they risk poor outcomes, including higher tax bills, fragmented estates and missed opportunities to protect family wealth. Advisers have a critical role to play in bridging this gap.

Clients’ fear of losing control is the primary barrier to effective planning. Traditional solutions, such as outright gifting or most trust structures, often involve surrendering access to capital. For many clients, that’s a deal-breaker.

One solution that addresses this challenge is Business Relief (“BR”). BR offers a way to mitigate IHT while maintaining access and control. It’s a solution that aligns with client priorities:

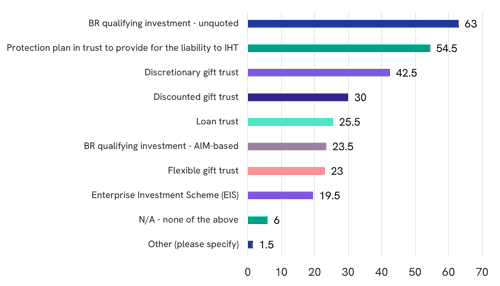

Our research shows that advisers recognise this. BR is now the most popular solution, alongside protection plans, as a route to mitigating IHT. While AIM-based BR faces headwinds post-2026, risk-managed BR solutions continue to offer full IHT relief.

So, what does this mean for advisers? Three practical steps stand out:

As pension reforms affect more clients, advisers are seeing greater demand for holistic long-term planning. The Budget changes and upcoming April 2026 reforms offer a natural prompt to revisit IHT, which is now a conversation that often includes beneficiaries as well as the client.

Concerns about complexity and uncertainty are common among clients. Setting out the different planning routes in plain terms, including the features that make BR more flexible than gifting or trust-based approaches, can help them make informed decisions.

Clients want control. Advisers want to close the advice gap. BR is the bridge between these two needs. It’s a tangible, flexible solution that helps clients act without feeling locked in.

Before opening new IHT conversations with clients, be ready to navigate the concerns most commonly raised: reluctance to give up control of assets (72.5%), a belief that planning can be left until later in life (65.5%) and uncertainty about future tax rules (50.5%). Build your recommendations in a way that directly acknowledges and resolves these worries.

We’re entering the most significant shift in estate planning in a generation. More clients than ever are drifting into the IHT net because of frozen thresholds, pension changes and rapid asset growth but most still aren’t taking action.

This creates a widening advice gap where client outcomes are at real risk and where advisers who lean in now will win deeper, longer, multi-generational relationships.

Download PDF version of the report

Source: Foresight data, survey of 200 financial advisers

This article is issued by Foresight Group LLP (“Foresight”) which is authorised and regulated by the Financial Conduct Authority (“FCA”) under firm reference number 198020 on 09/12/2025. Foresight’s registered office is at The Shard, 32 London Bridge Street, London, SE1 9SG. This article has not been approved as a financial promotion for the purpose of Section 21 of the Financial Services and Markets Act 2000 (“FSMA”).

This article is intended for information purposes only and does not create any legally binding obligations on the part of Foresight. Without limitation, this article does not constitute an offer, an invitation to offer or a recommendation to engage in any investment activity. The information contained in this article is based on material we believe to be reliable. However, we do not represent that it is accurate, current, complete or error free. Assumptions, estimates and opinions contained in this article constitute our judgement as of the date of the article and are subject to change without notice.

BR products designed to manage tax liabilities are not suitable for all investors and will place investors’ capital at risk, and you may not get back the full amount invested. The tax scenarios shown are indicative and are subject to change. Please note that the availability of the BR tax reliefs is dependent on each investor’s individual circumstances. BR tax reliefs are subject to change, investments may also rely on the company or investment opportunity in question meeting BR qualifying criteria which are not guaranteed.

Foresight does not provide financial, legal, investment or tax advice, and therefore potential investors should seek specialist independent tax and financial advice before deciding to invest. Past performance should not be taken as a reliable indicator of future results and forecasted returns are not guaranteed. The BR products are long term investments and you may not be able to get your money back out before the end of the investment term. Please see the relevant offering article for full details where attention should be paid to the risk factors set out.

This report is based on research conducted by Foresight Group in December 2025, surveying over 250 UK financial advisers to explore adviser sentiment, client behaviour, and the impact of regulatory change.