Real Assets

We build future energy systems and resilient infrastructure, backing emerging opportunities in technology, land and water.

The idea of satellite constellations as a disruptor is understandable. The number of LEO satellites has increased 127x in the past five years1. Yet despite the hype, towers remain the backbone of how we connect in a data-driven world. This article examines why that is the case, how tower companies generate revenue, and why the long-term fundamentals of the sector remain robust for investors despite the rise of new technologies.

Telecom towers are essential components of the mobile communications network. Each structure hosts antennas and radios that connect mobile devices to the wider digital ecosystem. When a person makes a call, streams a video, taps to pay, or loads an application, the signal is sent to the nearest tower, transferred through high-capacity fibre or microwave links, and then routed into the wider network.

Towers carry the overwhelming majority of global mobile traffic. They enable consistent signal quality, high bandwidth capacity, and reliable indoor and outdoor penetration. In practice, modern digital life depends heavily on the availability and density of tower infrastructure.

The business model behind towers is simple but powerful. Tower companies lease space on their structures to wireless carriers, who in turn deliver connectivity to billions of users worldwide. As individuals and enterprises consume increasing volumes of mobile data, carriers must continually expand network capacity. They do this either by adding radios and equipment to existing towers or by ‘densifying’ the network with new sites.

In both cases, utilisation of tower capacity rises. This enhances operating efficiency, increases tenancy ratios, and drives incremental earnings – an economic dynamic strengthened by the steady and persistent growth in global data demand.

Several features help explain why the sector continues to stand out:

Growth in mobile data traffic continues to be driven by more capable devices, increasingly rich content, and the ongoing digitalisation of economies. Unlike activity in more cyclical sectors, this growth persists independent of short-term technological hype and is expected to continue for the foreseeable future. Between 2024 and 2030, mobile data traffic is forecast to grow at a compound annual growth rate of 11%, with data usage per active smartphone rising from 19 GB per month in 2024 to more than 37 GB by 2030 (up from roughly 9 GB in 2020)2.

Carriers have consistently invested to keep pace with rising data demand and to improve network coverage, which remains a key driver of customer acquisition and retention. In the US alone, network capex has averaged around $23bn/year during the 3G era (2005–2009), increasing to $29bn/year through the 4G rollout (2010–2018), and is expected to reach $35bn/year between 2019 and 2025 to support 5G deployment3.

For tower operators, each incremental GB of data translates into capacity upgrades, higher tenancy ratios, and additional built towers. This steady, compounding revenue growth showcases the essential role of towers in meeting rising connectivity needs and highlights their importance as a long term, critical infrastructure asset.

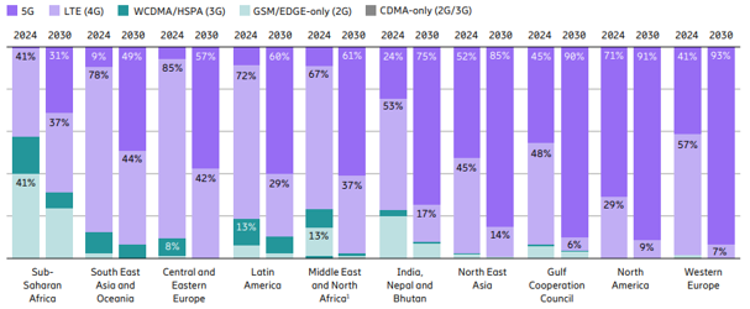

Furthermore, as the chart below highlights, there are regional differences in mobile technology adoption, indicating that many markets still have room to improve utilisation and operational efficiency as networks mature.

Mobile subscriptions by region and technology (percent)

Source: Ericsson Mobility Report 2025

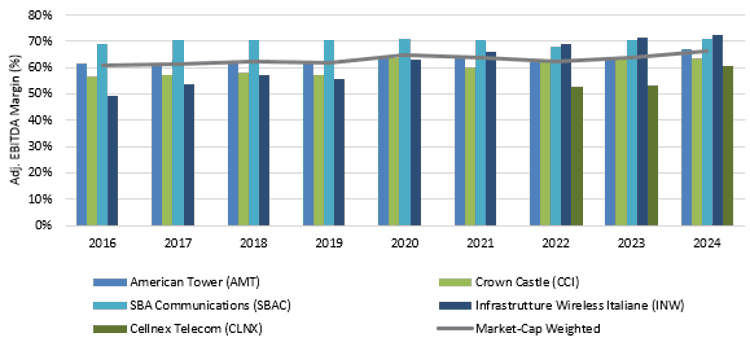

In mature markets such as North America and Europe, the tower industry benefits from limited new supply and constrained competition. Mobile network operators have already divested most of their tower portfolios, leaving only a handful of opportunities for new entrants. Where transactions do occur, new buyers often lack the scale, capital, or operational experience to compete effectively.

As a result, these regions have evolved into concentrated, oligopolistic markets, typically dominated by 2-3 major operators. On the public side, American Tower ("AMT"), SBA Communications ("SBAC") and Crown Castle ("CCI") are leaders in the US. Cellnex Telecom ("CLNX") and Infrastrutture Wireless Italiane ("INW") dominate the European market. American Tower stands out as a leading global player due to its scale and broad geographic footprint, making it a core holding within Foresight Capital Management’s (FCM) Infrastructure and Real Estate portfolios.

This disciplined market structure has enabled tower operators to generate robust and stable margins over many years.

Robust and stable margin profile reflecting infrastructure-like resilience

Source: FCM and Bloomberg

Telecom towers have also successfully adapted through every generation of mobile technology, from 3G to 5G, and continue to benefit as global data consumption accelerates. Telecom tower owners have proven to be a net beneficiary of technological advancements. Each network transition has expanded, not eroded, the need for reliable physical infrastructure. Their role as the final link between users and data remains central to mobile connectivity.

With companies like Starlink gaining attention, it’s easy to see why investors might wonder if the ‘sky’ could one day replace the ‘skyline’. Yet the reality is more nuanced: satellites are a complement to terrestrial networks, not a substitute.

Without getting too technical, LEO satellites operate between 500 and 1,500 kms4 above Earth, delivering latencies of around 20 to 50 milliseconds. GEO satellites, on the other hand, orbit much higher at around 36,000 kms, resulting in latencies of 500 to 700 milliseconds.5 For comparison, 4G networks typically have latencies of about 200 milliseconds, while 5G networks can achieve near-instant response times below one millisecond.6

Across urban and suburban areas, where most of the world’s data demand originates, satellites face the limits of physics. This includes weak building penetration, constrained capacity density, and higher operating costs. Moreover, a short useful life between 5–10 years and risks from orbital congestion add sustainability challenges. In contrast, tower infrastructure offers 20–30-year lifespans, minimal incremental costs, and long-term contracts that deliver the scalability and financial durability that satellites can’t match.

Satellites are clearly very valuable for connecting remote regions, but towers remain essential to the functioning of high-density, high-demand communication networks.

As digital infrastructure continues to evolve, satellites will no doubt play an important role in closing the world’s connectivity gaps through reaching places where towers may never stand.

Yet for the vast majority of global data transmission, the true enablers remain grounded. The same towers that have supported every generation of mobile technology continue to carry the world’s daily digital traffic, quietly supporting the connectivity we rely on far more than the satellites that capture headlines.

For infrastructure investors, the appeal of towers is clear: reliable, inflation-linked cash flows backed by the inevitable rise in data demand. In a world obsessed with what’s next, they remind us that value often comes from what already stands firm.

Sefa Degirmenci

Investment Associate

Foresight Capital Management

You have viewed 0 of 0

Foresight Group LLP does not offer legal, tax, financial or investment advice and the information on this website should not be construed as such. We recommend investors seek advice from a regulated financial adviser. The opportunity described in this document may not be suitable for all investors. Any such investment decision should be made only on the basis of the Fund scheme documents and appropriate professional advice.

Foresight Group LLP acts as investment manager and is authorised and regulated by the Financial Conduct Authority with Firm Reference Number 198020 and has its registered office at The Shard, 32 London Bridge Street, London SE1 9SG.

OEICs

An investment in FP Sustainable Future Themes Fund, FP Foresight Global Real Infrastructure Fund, FP Sustainable Real Estate Securities Fund, FP UK Infrastructure Income Fund or FP WHEB Sustainability Impact Fund and Liontrust Diversified Real Assets Fund (together the “Funds”) should be considered a long-term investment that may be higher risk. Portfolio holdings are subject to change without notice.

The Authorised Corporate Directors FundRock Partners Limited (registered office at Hamilton Centre, Rodney Way, Chelmsford, England, CM1 3BY) and Liontrust Investment Partners LLP (registered office 2 Savoy Court, London WC2R 0EZ), are authorised and regulated by the Financial Conduct Authority with Firm Reference Numbers 469278 and 518552 respectively. The Funds are incorporated in England and Wales.

ICAVs

An investment in the WHEB Sustainable Impact Fund and the WHEB Environmental Impact Fund (together the “Funds”) should be considered a longer-term investment that may be higher risk. Portfolio holdings are subject to change without notice.

The Manager of the Funds is FundRock Management Company S.A., authorised and regulated by the Luxembourg regulator to act as UCITS management company and has its registered office at Airport Center Building, 5, Heienhaff, L-1736 Senningerberg, Luxembourg.

We respect your privacy and are committed to protecting your personal data. If you would like to find out more about the measures, we take in processing your personal information, please refer to our privacy policy, which can be found at http://www.foresight.group/privacy-policy.